Proficient Auto Logistics (PAL)·Q4 2025 Earnings Summary

Proficient Auto Logistics Q4 2025 Earnings: Revenue Growth Amid Market Challenges

February 9, 2026 · by Fintool AI Agent

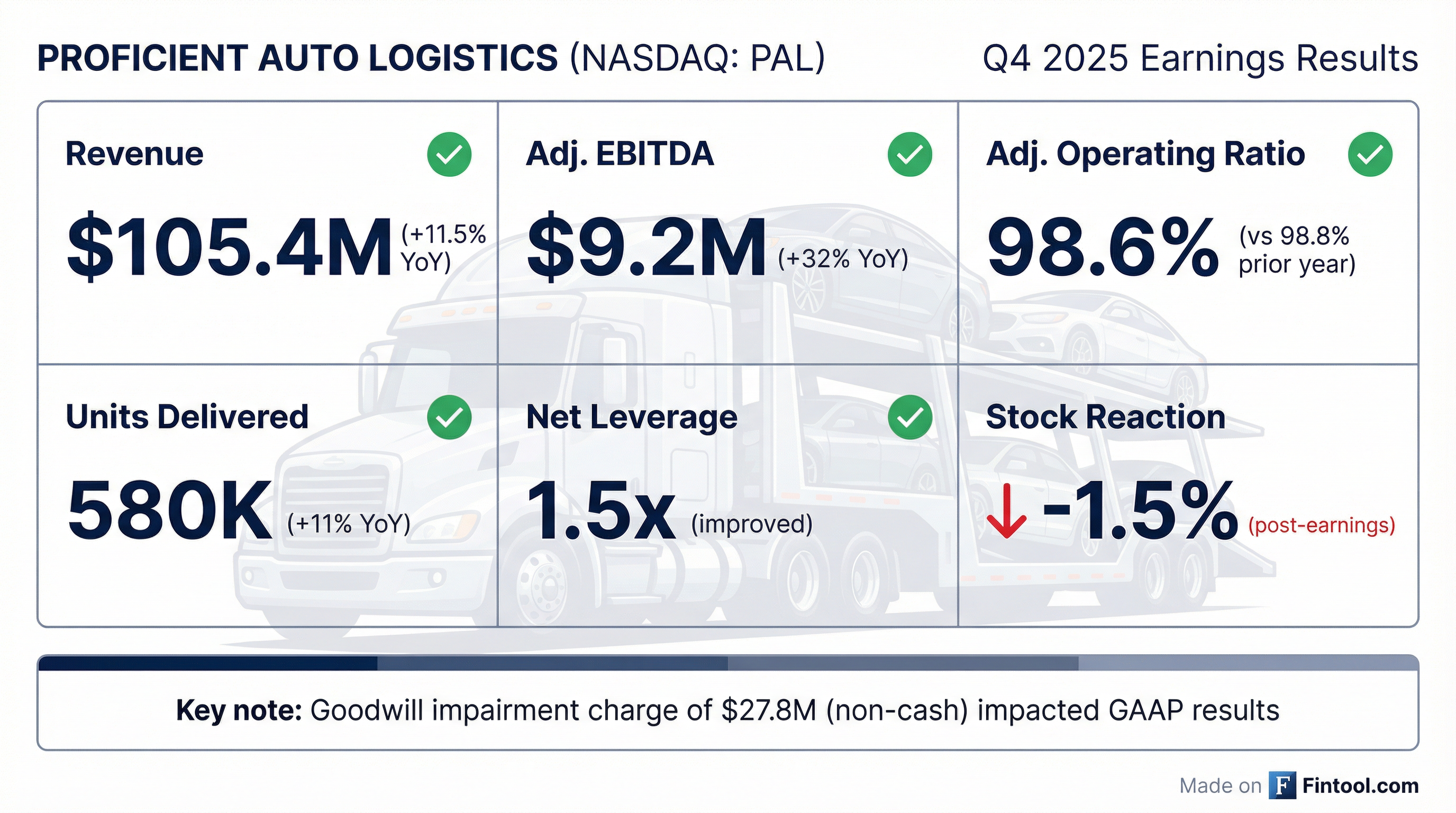

Proficient Auto Logistics (NASDAQ: PAL) reported Q4 2025 results that showed continued operational progress despite a challenging automotive market environment. Revenue grew 11.5% year-over-year to $105.4 million, while a $27.8 million non-cash goodwill impairment charge dominated GAAP results.

The auto transportation specialist delivered full-year 2025 revenue of $430.4 million (+10.7% YoY) and unit volumes of 2.31 million (+16.2%), demonstrating market share gains even as the broader automotive market weakened after peaking in March-April 2025.

Did Proficient Auto Logistics Beat Earnings?

PAL does not have significant sell-side analyst coverage given its small-cap status (market cap ~$291M) and recent IPO (May 2024). However, key metrics showed improvement versus year-ago results:

The GAAP operating loss of $(30.0) million was primarily driven by the $27.8 million goodwill impairment charge. Excluding this non-cash item, Adjusted Operating Income improved to $1.5 million from $1.1 million in Q4 2024.

What Caused the Goodwill Impairment?

The $27.8 million goodwill impairment was the result of annual impairment testing, which compared carrying value to estimated fair value using a discounted cash flow model.

CEO Rick O'Dell explained the context:

"The automotive market seemingly peaked in March and April ahead of tariff impacts, and the remainder of the year was weaker than our expectations."

The impairment reflects changes in market conditions relative to estimates at the time of PAL's IPO in May 2024. Importantly, this charge:

- Is non-cash and did not affect operating cash flows

- Did not impact Adjusted Operating Income or Adjusted EBITDA

- Reduced goodwill on the balance sheet to $148.5 million

How Did the Stock React?

PAL shares closed at $10.44 on February 9, 2026, down 1.5% following the earnings release. Key stock metrics:

The muted reaction suggests the goodwill impairment was anticipated given market conditions, and investors are focused on operational improvements and free cash flow generation.

What Changed From Last Quarter?

Improved Balance Sheet

- Net debt declined to $60 million (from $74 million at end of Q3)

- Net leverage ratio improved to 1.5x trailing twelve-month Adjusted EBITDA

- Debt reduced by $4.9 million during Q4 using strong cash flow

Market Share Gains Offset Weak Market

- Unit volumes grew +11% YoY despite automotive SAAR declining ~800K vehicles year-over-year in Q4

- The Brothers Auto Transport acquisition (completed April 2025) contributed a full quarter of revenue

- New business wins helped offset core market weakness

Integration Progress

- Completed integration of seven operating companies (five Founding Companies + ATG + Brothers)

- Established foundation for ongoing operating ratio improvement into 2026

Full Year 2025 Performance

The deterioration in adjusted operating ratio was impacted by the step-up in market value on fleet assets from IPO and subsequent acquisitions. Management noted this increased depreciation expense represents approximately 0.57% of the reported Adjusted Operating Ratio.

Key Operating Metrics

PAL operates one of the largest auto transportation fleets in North America, delivering vehicles from production facilities, ports, and rail yards to dealerships nationwide.

The shift toward company deliveries (37% of revenue, up from 35%) reflects management's strategy to increase utilization of company-owned truck assets.

Balance Sheet Position

As of December 31, 2025:

What Did Management Guide for 2026?

Management provided specific targets for 2026 despite a challenging market outlook:

CFO Brad Wright cautioned that the forecast for SAR is lower than 2025 actual, meaning:

"Any growth in our 2026 revenue and related profitability improvement is expected to be a result of our internal initiatives, essentially unaided by the general market."

January 2026 Update: Management noted January SAR may be the lowest monthly SAAR in several years due to severe winter weather disrupting dealership operations.

What Are the Key Cost Savings Initiatives?

Management identified several cost savings drivers for 2026:

CEO Rick O'Dell explained the margin opportunity from insourcing:

"We get better asset utilization of our fleet. We think that on an apples-to-apples basis, the OR on a company-delivered move is as much as 300-400 basis points better than on a sub-haul move."

How Is PAL Allocating Capital?

CFO Brad Wright outlined the capital allocation priorities on the Q&A:

"I think the priorities will be largely as they have been, which is to continue paying down debt... that does give us some flexibility and some dry powder to the extent that an M&A opportunity came along."

Capital Allocation Priorities (in order):

- Debt Paydown - Continue strengthening balance sheet (1.5x leverage now vs 2.2x in June)

- M&A - Pipeline active, one deal in progress, expect 1-2 acquisitions per year

- Share Repurchases - "Lower end of the priority list at this point"

Cash Flow Metrics:

- Trailing 12-month Adjusted EBITDA less CapEx: ~$30 million

- Free cash flow yield to market cap: ~11% (even after 60%+ share price increase in 3 months)

Q&A Highlights

Capacity and Pricing Environment

On non-domiciled CDL enforcement (Tyler Brown, Raymond James):

CEO Rick O'Dell noted the Interim Final Rule is now with OMB, and enforcement is increasing:

"For auto haul, we are lightly insulated there because we don't hire drivers who are new CDL recipients. We require drivers that have experience driving a large truck before they move into auto haul because it's specialized."

However, capacity exit is not yet impacting pricing because "the volume level is so low right now that you don't feel that capacity exit."

OEM Pricing Pressure

On carrier bidding behavior (Bruce Chan, Stifel):

"On the carrier side of things, we're seeing a lot of carriers with underutilized capacity... bidding at rates that, in many cases, are below a threshold that we think represents healthy reinvestment."

Management emphasized discipline in walking away from business when rates move below sustainable levels over a typical 3-year price term.

Contract Wins and Losses

On bid activity (Alex Paris, Barrington Research):

"We did pick up some new locations in a number of customer accounts. We also lost some incumbent locations in those same customer accounts, again, by virtue of rate dynamics."

Management noted some OEMs are rebidding lanes earlier than typical because carriers who won at aggressive rates are having service issues. PAL has positioned itself as the "carrier waiting in the wings."

Q4 OR Miss Explanation

On the insurance claims impact (Ryan Merkel, William Blair):

CFO Brad Wright explained the OR miss:

"We had one accident in the fourth quarter where we did have to basically reserve up to our full retention amount... the full retention that we have on our liability is $500,000, and we reserved all of that."

This $500K claims expense is not expected to recur in Q1.

Risk Factors to Monitor

- Automotive Market Weakness: SAAR trends directly impact demand for vehicle transportation

- Tariff Policy Uncertainty: Trade policy changes affect import volumes and OEM shipping patterns

- Driver Recruitment: Ability to recruit and retain qualified driving associates

- Acquisition Integration: Execution risk on integrating acquired companies

- Customer Concentration: Dependence on OEM contract business (93%+ of transportation revenue)

Earnings Call Details

PAL hosted an investor conference call at 4:30 PM EST on February 9, 2026.

- Webcast: Listen to replay

- Investor Contact: Brad Wright, CFO (904-506-4317)

CEO Rick O'Dell's closing remarks captured management's outlook:

"We grew revenue at 11%. As we continue to mature our network and focus on our cost initiatives, we've got a high level of confidence in our ability to improve our operating margins. In the meantime, cash flow is strong, balance sheet's improving. We like where we're positioned in the marketplace, but we just need the marketplace to be a little bit better. I think there are some sort of green shoots out there that could indicate that certainly the second half of 2026 can be better."

Proficient Auto Logistics, Inc. is a leading specialized freight company providing auto transportation and logistics services, operating one of the largest auto transportation fleets in North America.

Related Links: